July 16, 2026

Ask GPT about this BlogTop Payment Processors for Prediction Market Platforms in 2026

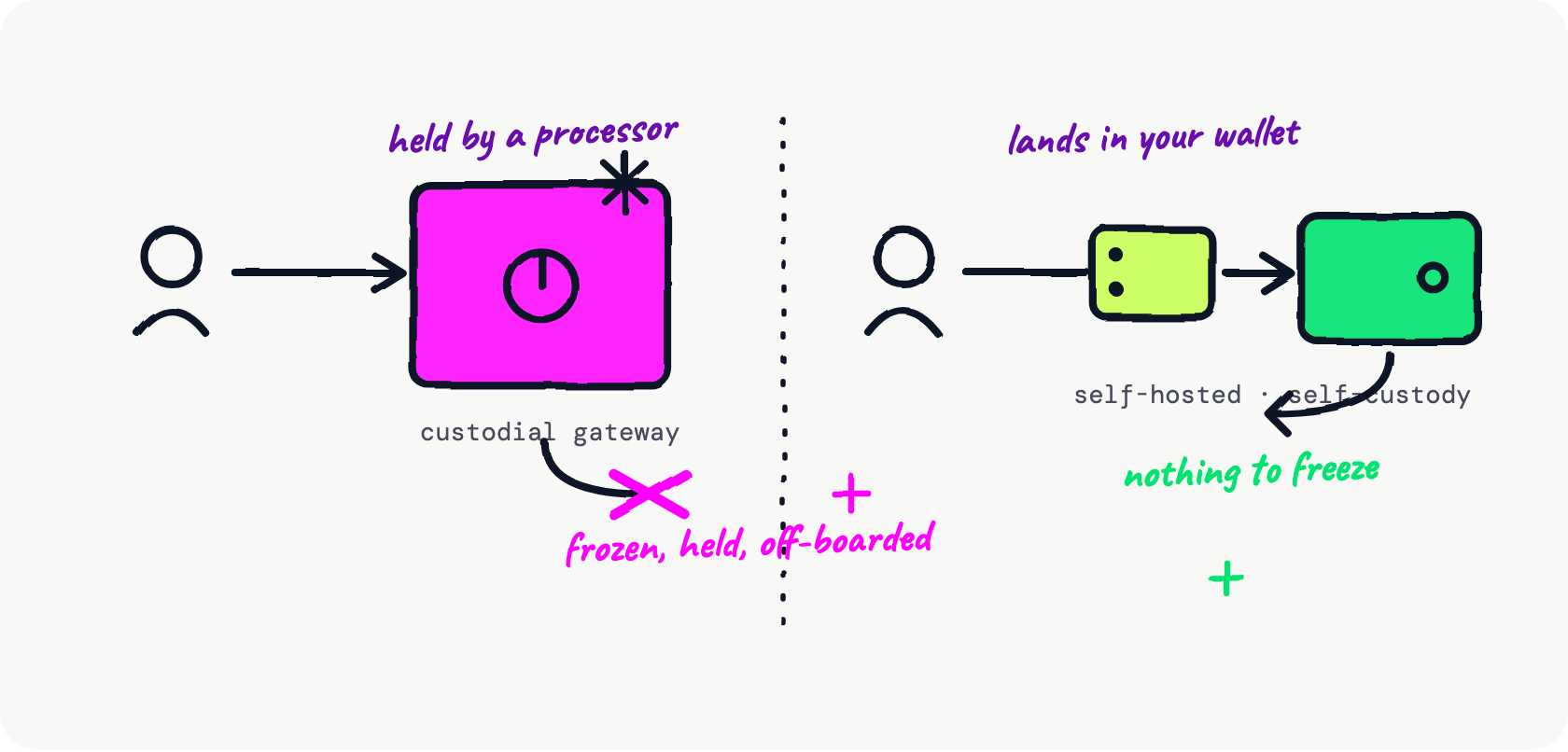

If you run a prediction market, your payment layer is not a checkout button. It is the thing a bank can freeze, a processor can off-board, and a regulator can ask about. Search "best payment processor for prediction markets" and every result is a consumer review of the Kalshi and Polymarket apps. This is the operator's version: an honest comparison of the rails you actually settle on. The short answer is that the real choice is not the fee. It is custody. A custodial processor holds your float and can freeze it. A self-hosted, self-custody stablecoin gateway lets deposits and payouts move straight through a wallet only you control.

This is a live decision because the category is exploding. Prediction-market volume climbed from under $5 billion a month in September 2025 to roughly $24 billion by April 2026, per Pew Research, and the first month of the 2026 World Cup pushed the sector past $50 billion in a single month, per CoinDesk. Kalshi raised at a $22 billion valuation in May 2026; Polymarket took a reported $2 billion investment from ICE at an $8 billion valuation in October 2025. More operators are launching, and each one has to answer the processor question before the first bet clears.

Operators are increasingly splitting into two camps. The regulated, fiat-first venues clear US dollars through banks and hold member balances in custody. The crypto-native venues settle in stablecoins on their own on-chain rails and never take custody of a user's funds. Which camp you belong to is mostly decided by your license and your market, and it decides which processors are even open to you.

Why prediction markets keep getting flagged high-risk

Card networks file betting under MCC 7995, "Betting, Casino Gambling, and Lottery," one of the most restricted merchant categories, the kind that requires explicit acquirer approval and dedicated merchant IDs. The trigger underneath is chargebacks. A losing bettor who disputes a card charge is textbook friendly fraud, and betting merchants blow past the network thresholds quickly. Visa's Acquirer Monitoring Program tightened its dispute-ratio ceiling toward 1.5% in some regions from April 2026, and Mastercard flags an "Excessive Chargeback Merchant" at a 1.5% ratio held for two consecutive months. Prediction markets clear those bars with room to spare.

Then there is the mainstream door, which is simply closed. Stripe's Restricted Businesses policy (updated May 2026) prohibits "Sports forecasting or odds-making with a monetary or material prize" outright, alongside "games of chance" and "internet gambling." PayPal's gambling policy bars "placing, accepting, recording, or registering bets." Neither names prediction markets, and neither has to, because the category is swept in by default. On top of that sits real regulatory uncertainty. As the law firm Holland & Knight framed the open question in February 2026, are sports event contracts "federally regulated derivatives subject to CFTC exclusivity" or "state-regulated gambling"? Underwriters price that uncertainty as risk, and risk shows up as higher fees, rolling reserves, or a declined application.

What operators are actually comparing

Consumer reviews compare deposit speed and app polish. Operators weigh something else. Across the teams launching platforms this year, the same five questions keep deciding the processor:

- Custody. Does the processor hold your money before you do? That is the surface a freeze, a hold, or an off-boarding acts on.

- Settlement speed. Do winnings and withdrawals settle in minutes, or on a T+1 to T+2 bank cycle that stalls over weekends?

- Chargeback exposure. Can a payment you already received be reversed against you later?

- Reserve and freeze risk. Will a slice of your revenue be held back for 90 to 180 days, and can the account be closed, as one common clause reads, "for any or no reason"?

- Data and reach. Who sees your customers' data, and can you take deposits and pay winners across borders without a correspondent bank in the middle?

How the two camps actually fund and pay out

The comparison gets concrete when you look at how the leading venues move money today, because each camp has trained its users to expect a different thing. The fiat-first, regulated camp settles in dollars and holds balances in custody. Kalshi funds accounts by ACH with no Kalshi fee but a multi-day settle, by debit card instantly at roughly a 2% processing fee, or by wire, and its crypto path runs through Zero Hash, where USDC or Bitcoin convert to US dollars on arrival. Member balances sit in custody. That is the price of the regulated, dollar-clearing model, and for a CFTC-designated venue it is the correct one.

The crypto-native camp does the opposite. Polymarket is non-custodial and settles in USDC on Polygon, takes a minimum deposit of about $3, accepts funds bridged from Solana, Base, Arbitrum, Tron, Bitcoin, or Optimism, and charges no deposit or withdrawal fee, so a user pays only cents of chain gas. Withdrawals go back out on-chain in minutes, any hour of any day. Limitless runs the same shape on Base, with shares collateralized one-to-one by USDC and same-day settlement. The behavior underneath is a global one: deposits skew small and frequent, and they come from users a card network barely reaches. On the broadest stablecoin rail, USDT on Tron, more than half of all transfers under $1,000 settle there, the everyday cross-border pattern these platforms plug into. A processor that fits the crypto-native camp has to match that: settle in stablecoins, pay out on-chain, and never make a winner wait on a bank's clock.

The 2026 processor comparison, from the operator's seat

The table below is built from each provider's own published pricing and custody model. It is deliberately operator-facing: the columns are the five questions above, not the consumer's deposit menu.

| Processor | Custody | Accepts | Payout & settlement | Chargebacks | Published cost |

|---|---|---|---|---|---|

| PayRam (self-hosted) | Self-custody. Funds land in a wallet only you control; no processor in the middle | BTC, ETH, TRX and USDC/USDT on Ethereum, Base, Polygon, Tron, plus a card-to-crypto onramp | Pays out stablecoins on-chain in minutes from your own wallet, weekends included | None. On-chain and final | Runs on hosting you own; commercial terms discussed privately |

| NOWPayments | Non-custodial (settles to your wallet), optional custody balance | 100+ cryptocurrencies | On-chain, near-instant; network-fee pass-through | None | 0.5% to 1% per transaction (NOWPayments pricing) |

| Coinbase Commerce | Non-custodial today (you hold the seed), but migrating merchants to the custodial Coinbase Business product | Major crypto and stablecoins | On-chain; about 2 seconds on Base | None | 1% per on-chain transaction (Coinbase Commerce) |

| BitPay | Custodial (BitPay holds, then pays out) | Crypto in, settles crypto or fiat | Daily settlement to your bank (about T+1 to T+2) | None on the crypto leg | 1% to 2% + $0.25; BitPay states "higher fees applicable for high-risk industries" (BitPay pricing) |

| CoinGate | Custodial or non-custodial (you choose) | Crypto and stablecoins | Weekly settlement by default | None | About 1% (CoinGate pricing) |

| High-risk fiat merchant account (PaymentCloud, Durango, Corepay) | Custodial, through an acquiring bank you do not control | Cards | Bank settlement cycle; payout holds possible | Your exposure and your cost | Quoted at underwriting; industry rolling reserves commonly 5% to 10% held 90 to 180 days (Merchant Maverick, SecureGlobalPay) |

Figures are each provider's own published pricing as of 2026. Network (gas) fees are blockchain costs paid to the chain, not to any processor. PayRam's commercial terms are set privately, case by case. This is a factual comparison, not an endorsement or a knock on any provider.

The pattern is hard to miss. Every custodial and fiat option carries the freeze surface, because the money passes through an account someone else controls. The non-custodial crypto gateways remove chargebacks structurally, because an on-chain payment is a push, not a pull. As the payments research desk at Spark put it in June 2026, "once the payer signs and broadcasts a stablecoin transaction, no third party can unilaterally reverse it, making friendly fraud structurally impossible." That single property erases the reason betting was high-risk to card rails in the first place.

Custodial vs non-custodial: the difference that actually decides it

This is the axis the consumer reviews never mention, so it is worth being precise. In a custodial gateway, the provider holds your balance and releases it to you on their schedule and their risk policy. That is the account a reserve is taken from and a freeze is applied to. The most cited example this year was outside prediction markets but instructive: a Shopify merchant reported a "$90,000 reserve hold" with "no response in 11 days," on 11,800 fulfilled orders and a 0.3% chargeback rate. The pattern, not the platform, is the point.

The industry's own direction underlines what is at stake. Coinbase is winding down its self-custodial Commerce product and moving merchants to a custodial "Coinbase Business" offering that, in its own description, holds a merchant's funds on their behalf. The default is drifting back toward custody, which is exactly the surface a freeze, a reserve, or an off-boarding acts on. A genuinely self-hosted, self-custody rail runs against that current on purpose.

Non-custodial gateways remove that account. There is one honest nuance to state plainly: stablecoins themselves carry an issuer freeze at the token-contract level. Tether reportedly blacklisted 4,163 addresses and froze roughly $1.26 billion in 2025. But there is a real difference between an issuer freezing a specific address tied to law enforcement and a processor freezing your entire float over an internal risk score. On a self-hosted gateway, each bettor gets a unique deposit address and funds land in a wallet you control, so there is no pooled account for a processor to hold, and no single address that carries your whole business.

Where a self-hosted stablecoin gateway fits, and where it does not

This is where PayRam sits, and it is worth being clear about what it is. It is not a processor you sign up with. It is software you run on your own server, live in about ten minutes, with no signup and no provider KYB. It is a dual gateway: it accepts deposits in BTC, ETH, TRX, and stablecoins (USDC, USDT) on Base, Polygon, Tron, and Ethereum, and it pays winnings out in stablecoins on-chain from a wallet only you control. Because the rails are crypto, pay-in and payout are cross-border by default. A bettor in Manila and a winner in Lagos settle the same way, in minutes, without a correspondent bank. There is no rolling reserve, no third party holding your float, and nothing for a risk desk to freeze. You can see the full model here, and operators building a multi-market business can run it in operator mode and set their own take rate.

One caveat matters more than any feature. A self-hosted crypto rail does not replace your license or your obligations. Whatever you operate under, a CFTC-designated contract market, an EU MiCA authorization, or an offshore gaming licence, you still own your KYC, AML, and reporting duties in your jurisdiction. PayRam is the settlement layer beneath that, and it keeps your compliance perimeter yours instead of handing it to a processor. Which model you can legally run, and where, is a question for qualified counsel, not a blog.

And the honest concession, because a comparison where one option wins every row is just an ad: a self-hosted crypto rail is not always right. If you are building a US-regulated venue that must clear in dollars, the Kalshi shape (bank rails plus custody) is what you need, and custodial fiat is unavoidable. If your users will not touch crypto at all, a fiat onramp still has to live somewhere. What changes with a self-hosted stablecoin gateway is only this: who holds the money in between, and whether a payment you already received can be taken back.

FAQ

What payment processor does Polymarket use?

Polymarket does not use a traditional payment processor. Per its own documentation, it settles positions in USDC on the Polygon network through a non-custodial proxy wallet (a Gnosis Safe with you as the single signer). Deposits bridge in as USDC and withdrawals go back out on-chain. There is no third party holding a user's balance.

Can prediction markets use Stripe or PayPal?

No. Stripe's Restricted Businesses policy prohibits "sports forecasting or odds-making with a monetary or material prize," which captures prediction markets, and PayPal's gambling policy is similar. This is why operators route to high-risk fiat accounts or to crypto rails instead.

Is a crypto payment gateway safer than a high-risk merchant account?

For the specific risks that hurt betting operators, yes. A high-risk merchant account still carries chargebacks, rolling reserves (commonly 5% to 10% held for 90 to 180 days), and the acquirer's right to freeze or close the account. A non-custodial crypto gateway removes chargebacks entirely, because on-chain payments are final, and a self-hosted one removes the pooled float a processor could freeze. It does not remove your own compliance obligations.

What does Kalshi use?

Kalshi is a CFTC-regulated exchange that clears in US dollars via ACH, debit, and wire, and safeguards USDC deposits in Coinbase Custody through a Zero Hash integration. It is custodial by design, which is exactly what its regulated, dollar-clearing model requires.

Reasoning Tree

Claim: For a prediction market operator, the payment processor decision is a custody decision, not a fee decision.

- Because betting is structurally high-risk to card rails (MCC 7995, chargebacks, regulatory uncertainty) → therefore mainstream processors like Stripe and PayPal prohibit it outright.

- Because on-chain stablecoin payments are push, not pull → therefore they cannot be charged back, which removes the core reason betting was high-risk.

- Evidence: Stripe's policy bars "sports forecasting or odds-making with a monetary or material prize"; high-risk fiat accounts commonly hold 5% to 10% rolling reserves for 90 to 180 days.

- Counterpoint: even non-custodial gateways face issuer-level stablecoin freezes → answered by self-hosting, where unique per-bettor addresses and a wallet you control leave no pooled float for a processor to freeze.

Bottom line: choose your rail by asking who holds the money and whether a payment can be reversed, not by comparing headline percentages.

Further reading

- How to accept USDC and USDT on a prediction market platform, the technical companion to this comparison.

- How to launch a prediction market platform, a payments-first guide.

- PayRam vs NOWPayments and the best crypto gateway for casinos and iGaming, adjacent high-risk verticals.

- Introducing PayRam Payouts, on paying winners in stablecoins no one can freeze.

If you want to see it running, you can deploy in about ten minutes or book a walkthrough.