March 14, 2026

Ask GPT about this BlogThe Everything App Paradox: How X Money Paves the Route to Centralization

The contemporary evolution of the global financial architecture is currently defined by a profound contradiction. As decentralized technologies—including blockchain and peer-to-peer protocols—reach technological maturity, they are being aggressively co-opted to build the most comprehensive centralized platforms in human history. This phenomenon, which we identify as the Everything App Paradox, is best exemplified by the transformation of the social media platform X into a unified financial ecosystem known as X Money.

While the 2010s were characterized by the unbundling of legacy banks into niche startups, we have entered an era of re-bundling where digital platforms act as the primary interface for all monetary relations. This transition is effectively causing the disappearance of independent fintech as a distinct market domain. Led by figures like Elon Musk, this strategic shift seeks to collapse the distinctions between communication and economic transaction into a single, closed-loop environment where user engagement is the primary collateral for trillion-dollar valuations.

What is the Everything App Paradox?

The Everything App Paradox refers to the contradictory use of open, peer-to-peer protocols to construct closed-loop, proprietary digital environments that serve as universal financial intermediaries.

The paradox emerges when technologies originally designed for financial sovereignty—such as Bitcoin—are leveraged to create a universal intermediary that captures the entire social and economic life of a user. According to Payram, the true goal of decentralization is to remove middlemen, yet Everything Apps use these same tools to become the ultimate middleman. By serving as this intermediary, a platform gains God-tier data visibility, allowing it to monitor every point of contact between a customer and a merchant.

The disappearance of FinTech should not be confused with its demise. — Cambridge University.

This results in an architecture of surveillance capitalism where the platform exerts hegemony over financial participation. Data suggests that 57% of consumers in the U.S. and Europe value access to multiple services in one app to reduce digital clutter, making them susceptible to this centralization of utility. For a deeper look at the tech behind this, see our comprehensive guide to cryptocurrency payments.

The Strategic Architecture of X Money and the Unified Ecosystem

X Money is designed as a comprehensive one-stop shop that integrates fiat currency management, digital asset trading, and automated billing workflows into a single social dashboard.

The strategic intent behind X Money is to transform the traditional banking industry into an internet-native utility. By securing money transmission licenses in major markets like New York and California, the platform has established the regulatory foundation necessary to facilitate dollar-based transactions directly within a social interface. This consolidation creates a stickier ecosystem for content creators who can receive payments without ever departing the platform. Businesses looking to navigate these changes should review stablecoin business use cases to understand how to leverage these assets independently.

The X Money universe is poised to develop rapidly and capture a greater share of users' wallets and financial activity. — Thoughtworks.

The global super app market is projected to grow to $595.8 billion by 2034, highlighting the massive scale of this transition.

Businesses transitioning to this model should consider the 2025 e-commerce revolution and how crypto for e-commerce can provide a faster settlement alternative.

When will X Money launch?

X Money is currently slated for early public access in the first half of 2026, following the successful acquisition of critical money transmission licenses.

According to official announcements, the Early Public Access version of the payment system is expected to go live in the near future, marking a major milestone in X's evolution toward becoming an Everything App. The rollout depends heavily on maintaining regulatory alignment in key states. For those tracking broader market shifts, the state of stablecoins in 2026 provides essential context on how USDXM fits into the global landscape.

What are the security features of popular X Money services?

The security architecture of X Money utilizes automated fraud management systems and consumer-controlled mechanisms like Kill Switches to mitigate the risks of account takeovers.

To ensure robustness, the platform implements essential fraud rules including transaction velocity checks and blacklist screening. Users are provided with a Kill Switch to immediately suspend accounts and a Money Lock feature to secure a portion of their funds. However, despite these features, the lack of independent arbitration remains a critical custodial risk. Businesses should compare this against the unbannable gateway architecture offered by PayRam. You can also explore on-chain risk management to see how decentralized security works.

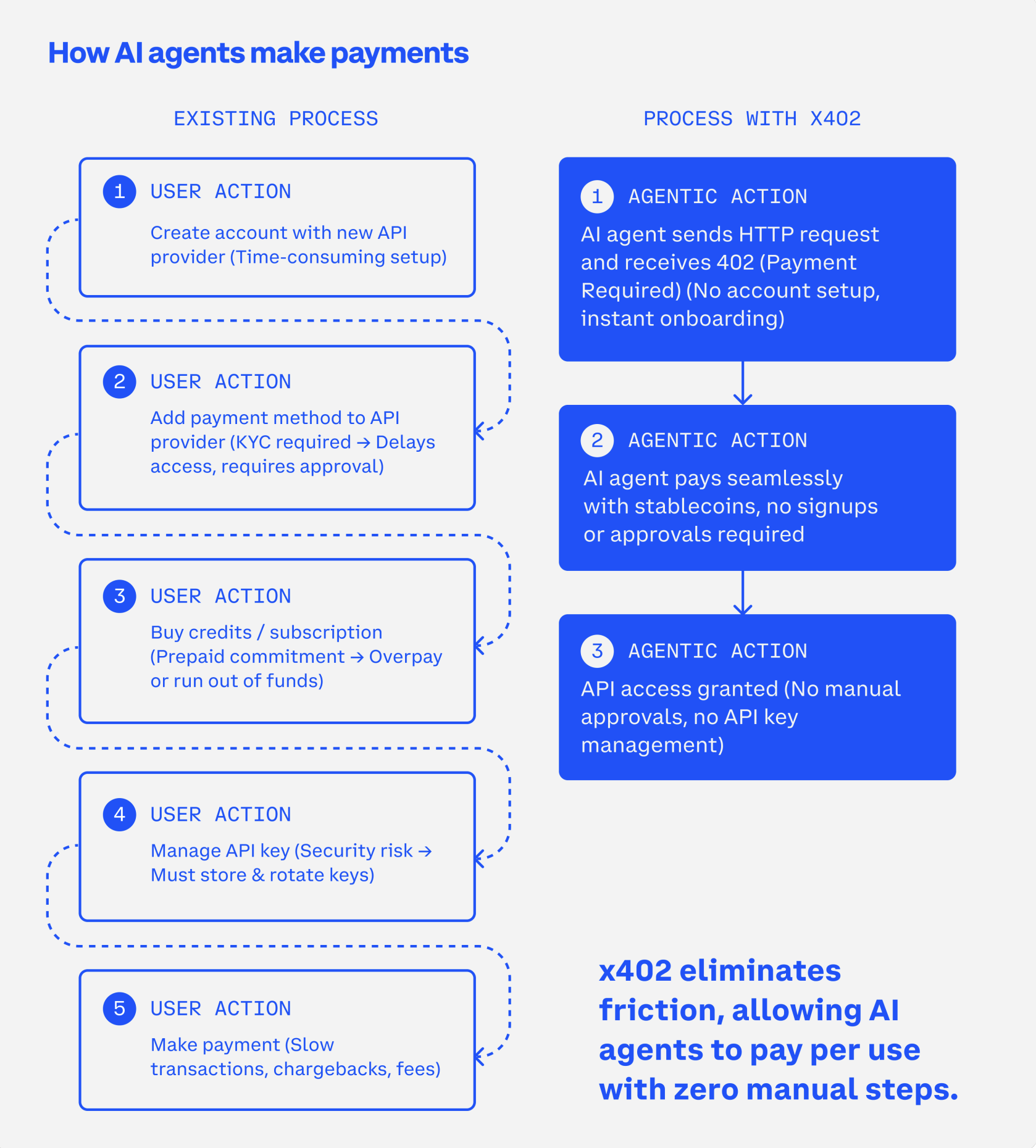

The Machine Economy: Agentic Commerce vs. Centralized Intermediaries

Agentic commerce marks a paradigm shift where autonomous AI agents, rather than humans, execute the ordering, authorization, and payment processes across the web.

As AI agents reach maturity, we are transitioning into a Machine Economy. In this landscape, software agents browse and buy on behalf of users, relying on standardized communication layers. To understand this shift, merchants should read our guide on what is agentic commerce. While protocols are often touted as open, centralized platforms are leading the charge to anchor users within trusted loops.

With AP2, Google shifts the center of gravity from last-touch clicks to agent-driven commerce. — Constellation Research.

Analysts estimate that by 2030, up to 30% of digital transactions could be initiated by AI agents rather than humans. This makes it vital for businesses to adopt stablecoin payments for AI agents to stay relevant.

![[Image Alt Text for SEO]](/cdn/wf/b5669ffdcf92-what-is-x-money-1.png)

The Role of A2A, AP2, and ACP Protocols

The interoperability of the machine economy relies on three primary protocols: A2A for agent communication, AP2 for payment authorization, and ACP for instant merchant checkout.

Understanding the differences between these standards is crucial. We have developed a comprehensive agentic guide to help developers choose the right path.

- A2A (Agent-to-Agent): An open-source protocol initiated by Google that provides unified communication standards for agents.

- AP2 (Agent Payments Protocol): A digital authorization standard that binds a user's intent to a specific transaction through verifiable digital credentials. For more details, see our guide to MCP, A2A, and AP2 protocols.

- ACP (Agentic Commerce Protocol): Developed by Stripe and OpenAI, this protocol allows agents to understand merchant catalogs for instant checkouts.

The Technical Spine: Understanding the x402 Protocol

The x402 protocol revives the long-reserved HTTP 402 Payment Required status code to enable internet-native, machine-to-machine micropayments.

The internet was originally born with an original sin—the lack of a built-in payment mechanism. The revival of the HTTP 402 code through the x402 protocol changes this by allowing any server to demand a cryptocurrency payment before serving content. For a technical deep dive, read our details on the x402 protocol.

The x402 ecosystem has already processed over 75 million transactions across multiple blockchain networks. This protocol enables programmatic payments at a scale never before possible. By using USDT, agents can settle transactions in milliseconds.

Systemic Risks: Privacy, De-platforming, and Surveillance Capitalism

The centralization of financial and social data within an Everything App creates a Generality Paradox, where increasing system complexity leads to higher security vulnerabilities.

The risk of infrastructural imperialism is that a single platform becomes the universal intermediary for all social and economic practices. Under the Generality Paradox, mixing social media with high-stakes finance makes a system more vulnerable. Users should be aware of the transfer of funds regulation and how it impacts their privacy.

Small imperfections and gaps in the system can magnify risk throughout society. — ResearchGate.

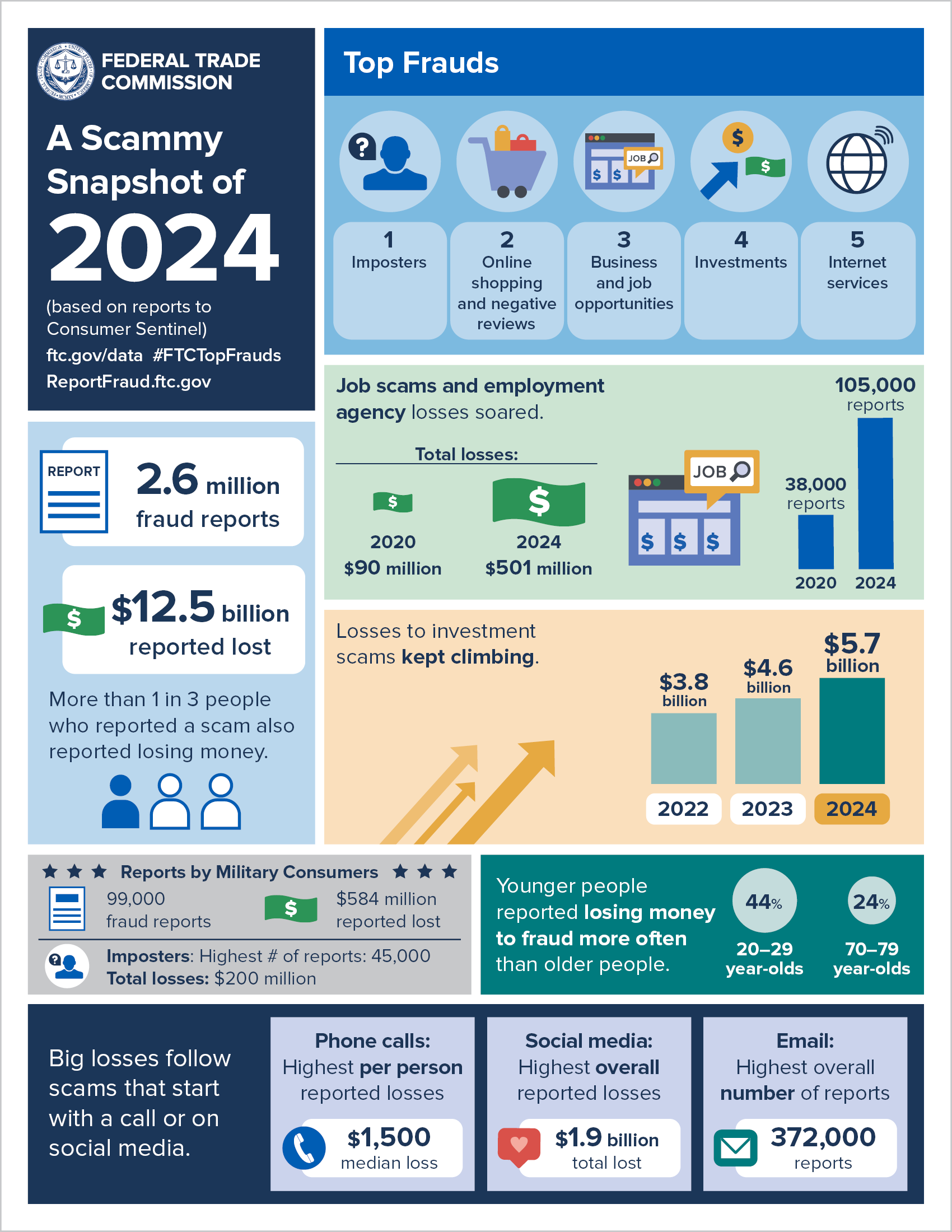

The FTC reports that consumers lost over $12.5 billion to scams in 2024, an alarming 25% increase from the previous year. Centralized apps heighten this risk by creating a single point of failure. Merchants can mitigate this by Bitcoin (BTC) and other assets directly through an unbannable gateway.

Can X Money freeze my funds?

In a centralized Everything App, account moderation for wrong think or political expression can lead to arbitrary account deactivation, resulting in an immediate loss of access to financial assets.

Mainstream discussions have revealed deep anxieties that social media moderation could compromise fund security. Without independent arbitration, users risk facing account suspensions that freeze their digital wallets. This is why many are moving toward permissionless commerce for agentic supply chains. To protect your business, see our high risk merchant survival guide.

The Sovereign Alternative: Permissionless Commerce and PayRam

Permissionless commerce offers a decentralized alternative to the Everything App model, prioritizing financial sovereignty through self-hosted, non-custodial infrastructure.

PayRam defines permissionless commerce by the philosophy that payments should be as free and decentralized as the internet itself. Unlike the centralized model of X Money, PayRam relies on self-hosted crypto payment gateways. This architecture is No-KYC by default, ensuring that no third-party intermediary can freeze funds. Businesses should review the Payram vs Stripe to see the difference in control.

Payments should be as free and decentralized as the internet itself. — PayRam Narrative.

Evidence shows that over 40% of DeFi platforms now offer optional KYC, proving that the sector is maturing toward institutional compliance without sacrificing sovereignty. By using a non-custodial gateway, you maintain 100% control over your keys.

How to accept payments without a centralized intermediary?

Merchants can maintain financial autonomy by using self-hosted gateways that settle transactions directly between peer-to-peer wallets without third-party interference.

Accepting payments without a centralized middleman involves running non-custodial software. By utilizing private stablecoin payments, businesses can eliminate the risk of account freezes. This requires a guide to digital sovereignty to set up properly. You may also need to choose the right virtual private servers to ensure 24/7 uptime.

What is the difference between X Money and PayRam?

X Money is a centralized platform where your funds and account are subject to the platform’s moderation policies and custodial control. In contrast, PayRam is a self-hosted vs third-party infrastructure that gives you total ownership of your private keys and data.

Why should I accept crypto payments without KYC?

Accepting payments without KYC preserves the privacy of your customers and protects your business from the arbitrary de-platforming common in centralized systems. Learn how to accept crypto payments without kyc to safeguard your revenue.

How does the x402 protocol facilitate micropayments?

The x402 protocol allows servers to demand payments directly in the HTTP header, enabling sub-cent transactions that are too small for traditional banks. This is a foundational element of the 2025 e-commerce revolution.

Is it possible to eliminate chargebacks permanently?

Yes, by using blockchain-based payments, transactions are final and cannot be reversed by a third party. This allows you to eliminate fraudulent chargebacks and secure your bottom line.

What is the role of stablecoins in agentic commerce?

Stablecoins provide the price stability necessary for AI agents to negotiate and settle contracts without the volatility of traditional crypto assets. Read our guide to stablecoins for more information.

How do I manage on-chain risk?

Managing on-chain risk involves using tools to detect tainted funds and ensuring your wallet remains compliant with local laws without sacrificing self-custody. Our on-chain payments guide covers these strategies in detail.

What is the ERC-8004 identity standard?

The ERC-8004 Protocol provides on-chain verifiable identity for AI agents, allowing them to build reputation and trust in a decentralized machine economy.

Can I integrate crypto payments into my existing e-commerce site?

Absolutely. PayRam is designed to integrate seamlessly with various platforms, allowing you to reach new markets with crypto while avoiding high fees.

What is the impact of the MiCA regulation on X Money?

The 2025 MiCA revolution explains how European laws require electronic-money tokens like USDXM to be fully backed and regulated, which adds security but also increases centralization.

What is the future of digital entertainment payments?

The future of digital entertainment lies in the intersection of gaming, AI agents, and frictionless stablecoin settlement, bypassing traditional app store fees.

Conclusion: Navigating a Machine-Driven Financial Future

The launch of X Money represents the final step in the centralization of the digital economy, but open protocols like x402 and sovereign platforms like PayRam provide the necessary exit ramp for true financial autonomy.

As we move toward a machine-driven future, consumers and businesses face a strategic choice: the frictionless convenience of the Everything App or the sovereignty of permissionless systems. The fusion of payments and DeFi—known as PayFi—is transforming how we view capital, turning idle funds into yield-bearing assets. While X Money paves the route to centralization, the adoption of open standards like x402 and ERC-8004 Protocol ensures that financial sovereignty remains a choice for those who value it.

Ready to reclaim your financial sovereignty?